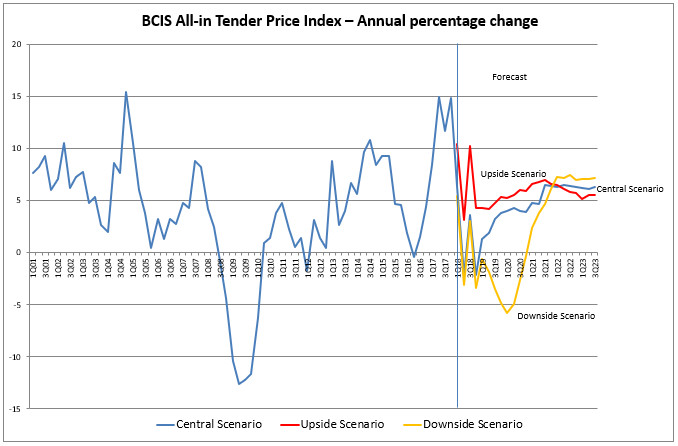

Over the next five

years (to 3Q2023) tender prices are expected to rise 29%.

Prices are forecast

to rise by an annual 3–4% over the first two years of the forecast, then rise

by 6 to 7% per annum over the remainder of the forecast period.

Building costs are

forecast to rise by 23% over the forecast period, by 3% over each of the first

two years of the forecast period, then by 5% per annum.

Over the forecast

period, construction materials prices are expected to rise by between 3% and 5%

per annum.

Average wage awards

are expected to be agreed at around 3% over the first two years, and then by

5–6% per annum over the final three years of the forecast period.

Output in 2018, as a

whole, is expected to remain flat compared with 2017, with a large fall in the

public non-housing sector and more subdued falls in the public housing and

private commercial sectors being balanced by increases in the remaining sectors.

A very modest recovery is expected in 2019, with output picking up in 2020, and

stronger output growth over the final three years of the forecast period,

driven in particular by very strong growth in the infrastructure sector. Over

the five years 2019 to 2023, new work output is expected to rise by nearly 25%.

A great deal of

uncertainty still exists over the years ahead for both the whole economy and

the construction industry. Little more light has been shed on how the exit

process from the EU will unfold, and there will probably be little more known

for another few months, with many different options being dependent on the

outcome of political votes, etc.

While almost any

outcome is still possible, BCIS will continue to produce forecasts based on

three scenarios. The results above are based on our central forecast.

The scenarios

reflect the different outcomes from the exit negotiations from the EU and are

equally likely. The uncertainty of the results of the Brexit negotiations will

undoubtedly lead to BCIS revising its assumptions again as more is known.

In all scenarios, it

is assumed that there will be no change of UK government over the forecast

period, and that there is political stability in the rest of the world. A

gradual rise in interest rates puts pressure on consumer spending.

Although a 'no deal'

is currently being discussed as an option, this may encompass a raft of

specific deals and has therefore increased the range of possible outcomes. A

specific forecast for this option has not been carried out.

However, the

likelihood is that a 'no deal' would tend towards our downside scenario.